Challenges

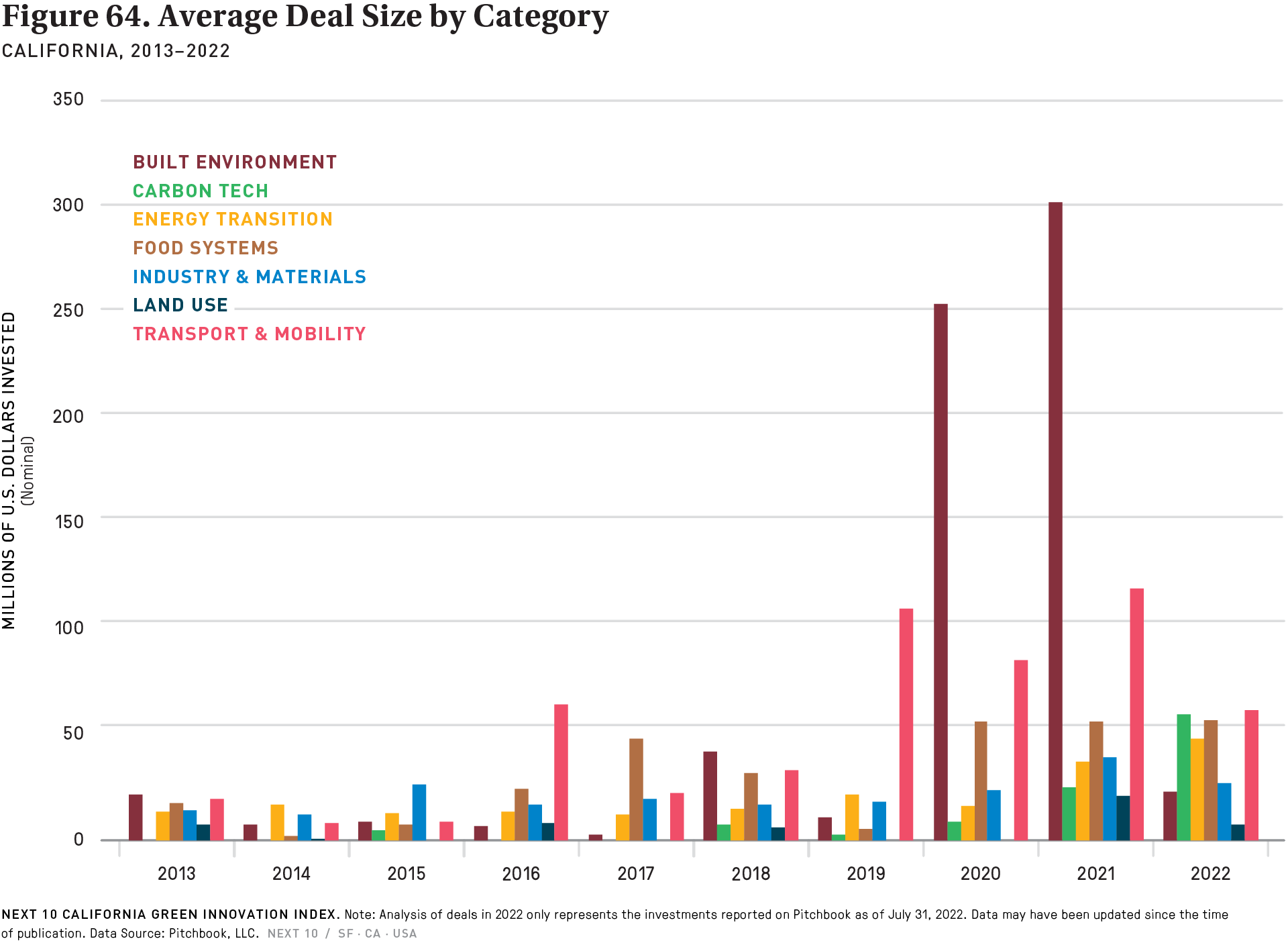

- Investment in transport and mobility firms sharply declined in the first half of the year. Only 1.58 percent of last year’s $21 billion had been raised as of July 31, 2022, and the sector has been slower to raise money than at any point since 2015. It did remain the largest target for investment, and its $342 million haul year-to-date would set records if it were raised in other states, but the drop-off in California is striking. Part of the dip is surely due to “regression to the mean” because last year’s megadeals by the likes of Rivian ($5.6 billion), Faraday Future ($4.2 billion), Bird Rides ($694 million), and Proterra ($693 million) pushed the sector to very large heights. Competition from other areas might be somewhat responsible as well.

- With 20 mobility deals completed this year, deal volume is only one-third of what it was last year. This means that the drop-off in mobility is not entirely related to megadeals. Again, there are signs that this is somewhat related to competition from other areas. In 2021, roughly one out of every three mobility deals were for a California company, and this year it is just 29 percent. With five deals each, Arizona and Florida had the second-most mobility deals.

Opportunity

- There is increasing investment in zero-emission vehicle (ZEV) firms headquartered in Southern California, with $243 million of the $342 million in mobility funding was raised by such ventures. Carlsbad’s Aptera led the way ($240 million), but there was also Hydroplane (Sherman Oaks, $2 million), Eli Electric Vehicles (Los Angeles, $1.93 million), and Ontario’s SAM of USA ($400,000). Most of these firms are involved in both the development and the manufacture of ZEVs, with the latter activity being a promising source of green, blue-collar jobs.199

199 Patrick Adler, Brady Allardice and Andrew Yu “Green the Golden Workforce: Progress and Pathways Toward Green Jobs Leadership

https://ucreconomicforecast.org/wp-content/uploads/2022/06/UCR_WP_Greening_Workforce_6_21_2022.pdf